If you’re a nurse feeling overwhelmed by your finances, you’re not alone. Many nurses are juggling multiple responsibilities, and financial management can easily slip through the cracks. Today, we’re diving into the two biggest financial burdens you may face: taxes and ignorance. Understanding these can empower you to take control of your financial future.

As a nurse practitioner with a side business, I recently realized just how complicated managing taxes can be. I finally hired a bookkeeper and a tax advisor to help me navigate this maze. The conversation we had about quarterly tax estimates opened my eyes to the reality that many of us face: taxes can take a hefty chunk out of our earnings. But what if I told you that being a W-2 employee often means you’re paying more in taxes than those with side hustles or businesses? Let’s unpack this.

The Tax Burden: W-2 Employees vs. Business Owners

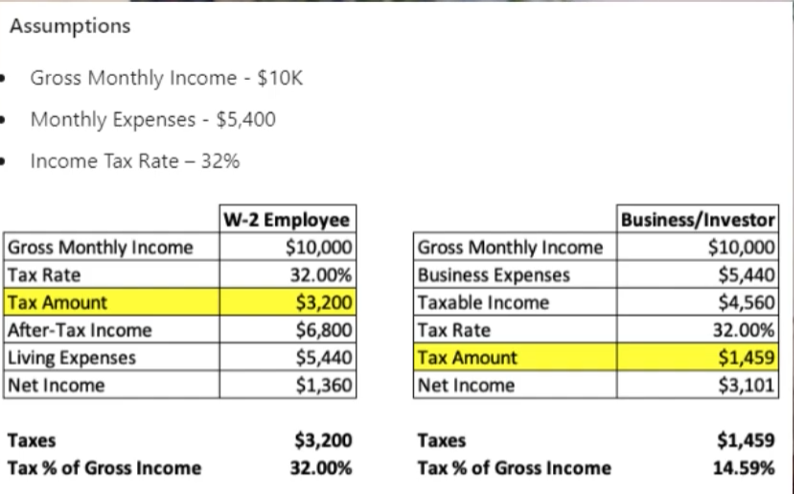

Did you know that W-2 employees are often the highest taxed individuals in the United States? It sounds shocking, but it’s true. When you’re earning a salary, your taxes are calculated based on your total income without considering your expenses. For instance, if you’re making $10,000 a month, you could find yourself in a tax bracket that takes a significant portion of that—potentially around 32%.

On the other hand, business owners and investors have the advantage of deducting their expenses before taxes are applied. If you’re running a side business, you can subtract costs related to that business from your income. This means your taxable income might only be a fraction of what you actually earn. For example, if you’re making $10,000 monthly but have $5,400 in business expenses, your tax burden could drop to around 14.59%.

So, what does this mean for you? If you’re a full-time nurse, it’s crucial to look closely at your paycheck. You might be surprised to find that nearly a third of your earnings are going straight to taxes.

Strategies to Lower Your Taxable Income

Now that we understand the tax landscape, how can you lower your taxable income as a nurse? Here are three strategies to consider:

- Invest in Pre-Tax Accounts: Contributing to retirement accounts like a 401(k) or a Health Savings Account (HSA) can significantly reduce your taxable income. These accounts allow you to set aside money before taxes are taken out, which can lead to substantial savings over time.

- Take Advantage of Tax Deductions: As a nurse, you may qualify for certain deductions related to your job. For instance, expenses incurred for continuing education or professional development can often be deducted. Always consult with your tax advisor to see what applies to you.

- Consider Side Hustles: While I don’t believe that everyone needs a side hustle to make ends meet, having one can open up additional avenues for tax deductions. Whether it’s freelancing, consulting, or starting a small business, these ventures can help offset your taxes and potentially increase your income.

Ignorance: The Hidden Expense

The second major expense that nurses face is ignorance—specifically, the ignorance of financial literacy. As I learned from a podcast by Alex Hormozi, ignorance can be the most expensive debt you carry. Imagine not knowing how to make your money work for you; that’s a costly mistake that many of us make.

When I started my nursing career, I didn’t invest a dime. I thought I was maximizing my income by keeping it all in my paycheck. Looking back, I realize that my lack of knowledge about investing cost me years of financial growth. If I had started investing early, I could be well on my way to financial independence by now.

So, what’s the takeaway? Investing in your financial education is the best investment you can make. It’s something no one can take away from you. Whether you’re in your 20s or 40s, it’s never too late to start learning and making informed decisions about your finances.

Conclusion: Take Control of Your Financial Future

In summary, the two biggest expenses for nurses are taxes and ignorance. By understanding how taxes work and taking proactive steps to lower your taxable income, you can keep more of your hard-earned money. Additionally, investing in your financial education can help you avoid the costly pitfalls of ignorance.

So, what’s next? I encourage you to take action. Consider signing up for my free class on stock market investing to learn how you can achieve financial freedom. Remember, education is your most valuable asset, and the sooner you start investing in it, the better off you’ll be.

Don’t let taxes and ignorance drain your resources. Take charge of your financial future today!