Are you a nurse in your 30s or 40s scrolling through Instagram, watching 22-year-olds flaunt their investment success? If so, you might feel like you’ve missed the boat on building wealth. But hold on! It’s time to stop that scroll and rethink your perspective. Contrary to popular belief, starting your investment journey in your 30s or 40s isn’t a financial disaster; in fact, it can be one of the best times to dive in.

As someone who didn’t invest a single dollar until I was nearly 30, I understand the hesitation. My name is Elaine, and I’m a financial educator and nurse practitioner with over 15 years in the field. My mission is to help nurses like you turn your hard-earned degrees into wealth-building machines, freeing you from the confines of endless bedside shifts. In this article, I’ll share why investing in your 30s and 40s can be your secret weapon for financial success.

Is It Too Late to Start Investing?

Every week, I receive messages from nurses in their 30s and 40s expressing doubt about starting to invest. Many believe they are too old to learn about the stock market or index funds. Let me be clear: it is never too late to start. If you’re feeling guilty about not investing earlier, you’re not alone. I carried that guilt for years, but I want to share a different perspective with you.

My Journey: From Financial Guilt to Empowerment

When I graduated nursing school at 21, I was fortunate to have no student loans. However, my entry-level salary of around $28 per hour in California left little room for saving or investing. Like many young professionals, I was more focused on enjoying life—traveling, dining out, and even leasing a flashy two-door car that cost me nearly $800 a month. Investing was nowhere on my radar.

It wasn’t until I was pregnant with my first child in my late 20s that I felt the urgency to become financially responsible. I began to educate myself about investing, but the guilt of not starting earlier lingered. I often saw online calculators showing how much wealth I could have built by starting at 22, and it made me feel sick. But here’s the twist: I realized that the narrative surrounding early investing is incomplete.

The Myth of Early Investing

Many financial gurus promote the idea that the only path to wealth is to start investing young, with money you didn’t have and knowledge that was never taught to you. This narrative ignores the reality that most of us, especially nurses, come from backgrounds where financial literacy was not a priority.

Feeling behind can paralyze you and prevent you from taking action. But here’s the truth: your 30s and 40s can actually be your superpower in investing. Let’s explore three compelling reasons why.

1. The Wealth-Building Gap

In your 20s, it’s common to scrape by with minimal savings. For example, I was thrilled if I had $50 left at the end of the month. Fast forward to my 30s, and as a nurse practitioner, my income had significantly increased while my expenses remained relatively stable. This created a wealth-building gap—the difference between what you earn and what you spend.

For many nurses, this gap can widen dramatically as they transition into higher-paying roles or take on additional shifts. While you may have only been able to invest $20 a month in your 20s, you might find yourself capable of investing $800, $1,000, or even $1,500 a month in your 30s. The volume of your investments can far outweigh the advantage of starting earlier.

2. A Shift in Mindset

In your 20s, retirement may feel like a distant concept. You’re living for today, enjoying life with friends and family. However, as you enter your 30s and 40s, your priorities shift. You start thinking about your future and the desire to avoid being stuck at work at 60. This newfound clarity about your financial goals fuels your motivation to invest.

When you understand your “why” and have a clear vision of what you’re building towards, discipline becomes easier. This focus is often lacking in younger investors, who may not yet grasp the importance of long-term planning.

3. Enhanced Tax Advantages

As your income grows, so do the tax advantages of retirement accounts. Contributing to a 401(k) or an HSA becomes more beneficial as you enter a higher tax bracket. You can take advantage of tax-deferred growth and potentially pay less in taxes on your contributions compared to your 20s.

This means that the tools available to you in your 30s and 40s are often more powerful than those available to younger investors.

Crunching the Numbers: A Real-World Comparison

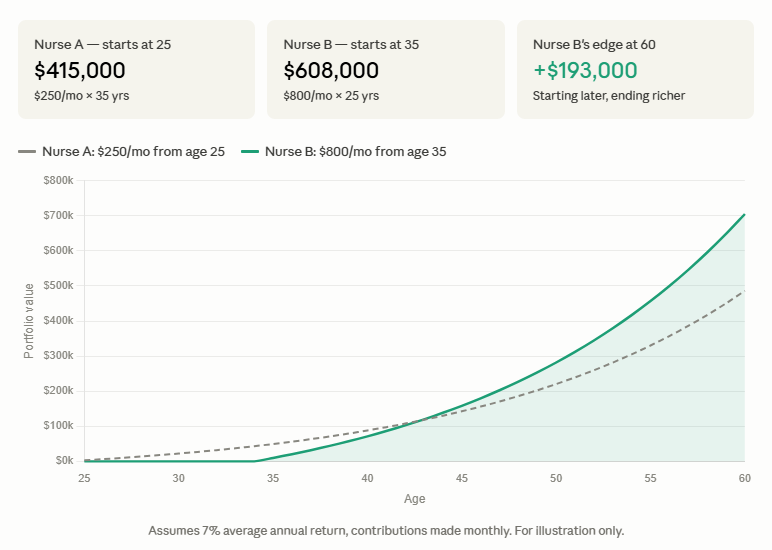

Let’s break this down with a simple example. Consider two nurses: Nurse A starts investing at 25, contributing $250 a month for 35 years at a 7% average return. She ends up with approximately $415,000 at retirement.

Now, Nurse B (that’s you!) starts investing at 35, contributing $800 a month for 25 years at the same 7% return. Nurse B ends up with nearly $680,000—almost $200,000 more than Nurse A, despite starting 10 years later.

This illustrates a crucial point: higher contributions can significantly outpace the benefits of starting early. The narrative that you’re behind simply doesn’t hold up against the numbers.

Actionable Steps for Financial Freedom

If you’re in your 30s or 40s and feeling like you’ve missed your chance to invest, here’s what you can do this week:

- Check Your Employer’s Retirement Account: Look into your 401(k) or 403(b) and ensure you’re taking full advantage of any employer match. If you’re not contributing enough to get that match, you’re leaving free money on the table.

- Open a Roth IRA: If you don’t have one yet, open a Roth IRA. It’s an excellent retirement account for those with earned income. Start with whatever you can—$50, $100, or more. The goal is to get started and build the habit of investing.

- Assess Your Wealth-Building Gap: Review your last three months of bank statements to understand your income and expenses. Calculate what’s left over. This surplus is your starting point for investing, no matter how small.

Conclusion: Start Now!

If you’re in your 30s or 40s, I want you to know that you are not behind. You’re exactly where you need to be, and today is the perfect time to start investing. Remember, yesterday was better, but today is the next best option.

The only thing standing between you and financial freedom is the decision to start. Don’t let age or past decisions hold you back. Whether you’re in your 20s, 30s, or 40s, the time to act is now.

Share your starting age and what’s holding you back from investing in the comments below. You’re not alone, and together we can navigate this journey to financial freedom. If this article resonated with you, subscribe for more insights on building wealth without burning out.

Let’s take this journey together!